Nov 21 was the day that Ireland finally stopped battling the waves and took the EU's money, joining Greece in the naughty step of protectorate-dom and plunging into an abyss of political instability. And there is worse news closer to home: turns out Greece won't be getting additional time to pay off our EU/IMF loans as it turns out those nasty Germans don't like the thought of us defaulting on their claims so early in the game.

The bailout of course failed to put anyone at ease regarding the fate of the rest of the European periphery. It did however cheer up big government apologists in Greece and elsewhere, who are already chanting the moral of Ireland's story: that austerity is self-destructive as it couldn't save the IMF's star pupil, that low taxes

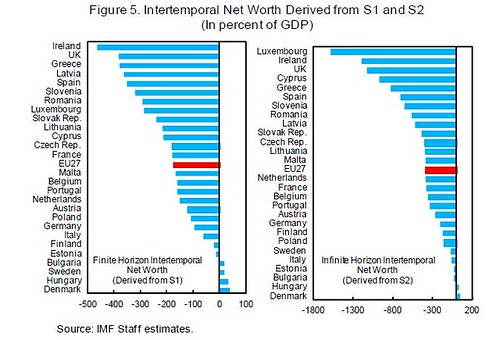

They are right almost as much as they are wrong. In Greece and Ireland, banking on a crash course of austerity on the IMF's terms to get our economy growing again and bring our debt down was never going to work because both countries were clearly insolvent. The IMF death list can be seen clearly on the left below:

Technically, the UK should also have followed us into the bottomless pit by now but they have their own currency and central bank which does allow them a bit of leeway - perhaps enough for them to avoid a default but who knows?

With the UK temporarily out of the way the next EU member on the IMF's stochastic death list is Spain. Now the Spaniards will argue until they are blue in the face that they aren't Ireland or Greece but actually they combine the worst of both worlds - sharing as they do both Greece's hideously sclerotic labour market and Ireland's property-obsessed cult of suicide bankers. The only way in which they are unlike the previous two is that Spain is very, very large - so large in fact that the EU bailout fund cannot save it.

On the other hand, Portugal might be next. They are technically much better off than Spain (i.e. ranked lower on the death list) but they might attract more attention as they are a smaller country and because point-scoring politicians in the Portuguese opposition have just hit the market with some scary numbers. Always a bad idea putting numbers to bad news. It makes people reach for their excel sheets and update their models.

What people refuse to understand about the chain of sovereign defaults is that it isn't troubled European countries that are defaulting - it's the whole system. Spain will not be saved because its debt is 'only' 53% of GDP as opposed to Ireland's 65% or Greece's 127%. The simple truth is that no one believes Europe can grow fast-enough, in a credit-constrained world and without irresponsible levels of government spending, to get itself out of debt. One can spend all day arguing that a jet fighter is faster than a DIY Red Bull Flugtag plane or a seagull, or that one weighs more than the others, but all three must eventually come down because none of them can reach escape velocity.

Until three years ago, the consensus was that European sovereigns could not default, period. Last year, the consensus became that European sovereigns could never really default, except through inflation. Earlier this year, it became 'clear' to us all that the periphery could indeed default. Now markets are waking up to the fact that even larger and 'safer' European sovereigns could default. Portugal is, as per the Death List, more solvent than France and much more solvent than the UK. It's only market participants' superstition and their love of guarantors that is keeping them from betting on the obvious.

Back to the IMF for a second. Given that it compiled the Death List in the first place, surely the Fund (or its staff) know what's going on, even if they can't admit it in review after review of our adjustment mechanism?

Perhaps this paper written by the IMF's own staff is meant to give us a hint.