Very few analyses of the Greek fiscal situation and the inevitable default discuss demographics, which I find frankly baffling. The typical defaulting country is young (see my Greece vs Argentina comparison here). Greece is patently not. Some people think this changes nothing but it changes absolutely everything.

First of all, let's get a few things straight. Demographics can't be talked around. The ageing of Greece's equivalent to the baby boomers is going to happen regardless of whom we vote in to manage it, and regardless of what mandate we give them. (Except perhaps Kill Grandma!). It is a tectonic shift; a force of nature; the wrath of god. As you can see from my friend Diego's comments below, the same forces are at work in Spain; Portugal and Italy aren't far off. In fact, the only exception is Ireland... for now.

Simply put, Greeks are living to a ripe old age, which is fantastic. Long may it continue. But there is a price to pay, and we will pay it in two ways.

The first of these is the complete PWNAGE of the assumptions built into the social security system. Remember, actuarial projections tend to be done on a 50-year basis (see here), so if you get your assumptions wrong, things can get out of hand very quickly. And assumptions were off indeed in the past. In fact, mortality was assumed under EU guidelines to be 33% higher than the ILO would have recommended. This is money that should have been set aside for grandma's old age but was not because she wasn't expected to live to that age. We were literally keeping our fingers crossed, knuckles white, that grandma would die so we wouldn't have to fork out her pension money. Even so, by 2009 the bill for caring for the elderly had reached EUR27.3bn, not counting any health-related spending on older patients. My best guess based on the correlation between the two is that that would be another 2bn per annum. Older Greeks' share of the population is growing in an almost linear fashion [See graph on SeekingAlpha]. Payouts on pensions in Greece (other than private policies) have grown much faster than the Eurozone average (source); this is the third fastest growth rate in Europe, surpassed among others by fellow PIIG Portugal.

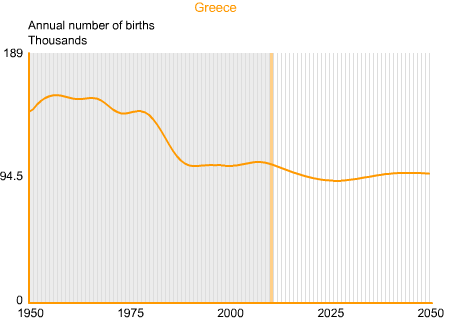

On top of this, fertility in Greece looks like it fell off a cliff going into the 80s (although you may want to look at the very detailed note left below by a helpful contributor and my much more detailed look into the matter here) and never recovered, despite the best efforts of immigrants. There's a number of reasons for this, reviewed here, but essentially, the nation's values and lifestyle had been changing beyond recognition for decades. The 80s only really marked a more decisive turning point. See the trajectory of fertility below (Source UN Statistics Division and INED via Seeking Alpha), although I should note there are alternative forecasts of fertility (H/T @Geo_Gem) which are more optimistic, on the assumption of consistent migration patterns. Which won't happen because of this.

First of all, let's get a few things straight. Demographics can't be talked around. The ageing of Greece's equivalent to the baby boomers is going to happen regardless of whom we vote in to manage it, and regardless of what mandate we give them. (Except perhaps Kill Grandma!). It is a tectonic shift; a force of nature; the wrath of god. As you can see from my friend Diego's comments below, the same forces are at work in Spain; Portugal and Italy aren't far off. In fact, the only exception is Ireland... for now.

Simply put, Greeks are living to a ripe old age, which is fantastic. Long may it continue. But there is a price to pay, and we will pay it in two ways.

The first of these is the complete PWNAGE of the assumptions built into the social security system. Remember, actuarial projections tend to be done on a 50-year basis (see here), so if you get your assumptions wrong, things can get out of hand very quickly. And assumptions were off indeed in the past. In fact, mortality was assumed under EU guidelines to be 33% higher than the ILO would have recommended. This is money that should have been set aside for grandma's old age but was not because she wasn't expected to live to that age. We were literally keeping our fingers crossed, knuckles white, that grandma would die so we wouldn't have to fork out her pension money. Even so, by 2009 the bill for caring for the elderly had reached EUR27.3bn, not counting any health-related spending on older patients. My best guess based on the correlation between the two is that that would be another 2bn per annum. Older Greeks' share of the population is growing in an almost linear fashion [See graph on SeekingAlpha]. Payouts on pensions in Greece (other than private policies) have grown much faster than the Eurozone average (source); this is the third fastest growth rate in Europe, surpassed among others by fellow PIIG Portugal.

On top of this, fertility in Greece looks like it fell off a cliff going into the 80s (although you may want to look at the very detailed note left below by a helpful contributor and my much more detailed look into the matter here) and never recovered, despite the best efforts of immigrants. There's a number of reasons for this, reviewed here, but essentially, the nation's values and lifestyle had been changing beyond recognition for decades. The 80s only really marked a more decisive turning point. See the trajectory of fertility below (Source UN Statistics Division and INED via Seeking Alpha), although I should note there are alternative forecasts of fertility (H/T @Geo_Gem) which are more optimistic, on the assumption of consistent migration patterns. Which won't happen because of this.

{kind=link}

{kind=link}

That's part one, but it's not the greater change.

Age changes everything. Older people draw down savings to finance their consumption. They are less likely to chase after jobs. They are less likely to retrain. They work, spend and vote differently. They are much more likely to, let's face it, just die.

Let's start with the spending bit. It's pretty simple to see how age changes consumer behaviour as there are some handy statistics to call upon. Try this table for example. Sure the data are a little dated (2005) but ageing is not a new process so I suspect the key findings will remain the same. At any rate, the graph below shows how much more or less the typical adult equivalent (i.e. either one adult or a minor 'scaled up') consumes in a household where the reference person (typically the head of the household) is 60 or over, versus one where the reference person is 45 to 59. I focus on the latter because they are the main earners and the wealthiest among the Greek population, so how they spend their pennies tends to matter more than how students do.

Let me give you a few hints on what this means. It means the Greek market for drugs and medical treatment will boom. It means the national electricity corp. is worth more than some people think. It means the usual route out of unemployment will soon be as a maintenance/repairman, a cook or a waiter, as opposed to a retail salesperson or clerk. It also means that, long-term, steadily ramping up taxes on alcohol is likely to make more money than taxing tobacco.

You know how the Greek government expects 1bn per annum in VAT from tobacco sales alone? Well the over 60s tend to spend 39% less on tobacco than the 45 to 59ers. When the Greek government tries to sell our Electricity company, they may want to remind prospective buyers that an ageing population is good for them, as the over 60s spend 43% more on fuel than the 45 to 59ers. Of course it will probably spend the increased fuel tax revenue (we expect 7.65bn per annum in various fuel taxes) subsidising shivering grandmas, so better not count on that money. Selling OTE, on the other hand, might be an issue as the over-60s spend 20% less on telecoms than the immediately younger group. The list goes on and on.

More analysis to come.